Book Chapter: A Decade of Steady Economic Decay

Authors – Ajay Bisaria, Abhishek Kumar

Abstract

This piece analyses Pakistan’s persistent economic challenges, particularly in the decade from 2013 to 2024. It links the country’s financial crises with structural weaknesses, primarily military dominance, that has led to political instability, flawed economic choices and an addiction to IMF bailouts. The economic crisis has aggravated from 2021, since when the Pakistani rupee has depreciated drastically, inflation surged, GDP growth stagnated, and foreign reserves plunged.. The failure to implement tax reforms, fix chronic energy sector inefficiencies, or to attract foreign direct investment (FDI), together with populist schemes, have further exacerbated economic instability. The military’s control over key industries and excessive defence spending have diverted resources from essential development. The article highlights Pakistan’s cyclical dependence on IMF’s Extended Fund Facility (EFF), noting how successive programs in 2013, 2019, and 2024 provided temporary relief but failed to address deep-rooted economic problems. While the 2024 EFF emphasizes climate resilience and digital transformation, Pakistan remains trapped in a cycle of debt and economic stagnation, without deep structural reformssuch as broadening the tax base, privatizing inefficient state-owned enterprises, and reducing military influence.

Introduction: An Imploding Economy

Pakistan’s economy has faced profound challenges in recent years, driven by continued mismanagement that has stifled growth and stability. According to Topline Securities, the Pakistani rupee has undergone severe devaluation, with an average annual decline of 10 percent in nine consecutive years, to 279 PKR against the US dollar in 2024 [1]. This depreciation drastically inflated the cost of critical imports such as energy, machinery, and pharmaceuticals, exacerbating trade deficits and draining foreign exchange reserves to 10.7 bn USD in 2024, barely enough to cover 2 months of import [2]. As a consequence, according to the Pakistan Bureau of statistics, the GDP growth rate contracted to -0.2% in 2023, (and was an estimated 2.5 percent in 2024), reflecting stagnation across key sectors like agriculture, manufacturing, and services. Simultaneously, inflation surged to 23.4% in 2024, driven by rising food, fuel, and utility prices, pushing millions below the poverty line. The World Bank estimates that over 40% of Pakistanis now live in poverty, with household purchasing power eroded by stagnant wages and unemployment rates exceeding 8%.

Political instability and security crises have further destabilized the economy. Frequent changes in leadership, contentious elections, and bureaucratic inefficiencies have disrupted policy continuity. At the same time, security challenges including the resurgence of the Tehrik-i-Taliban Pakistan (TTP) and the Balochistan Liberation Army (BLA), have heightened the security risks, deterring foreign investors and tourism. Foreign Direct Investment (FDI) plummeted by 35% in 2021 [3], with critical infrastructure projects delayed or abandoned.

In response, Pakistan pleaded again, particularly after a caretaker regime arrived in 2022, for external assistance from the International Monetary Fund (IMF), as the reliable lender that has bailed out the economy for decades. After tough negotiations across civilian regimes, the IMF approved its 7th Extended Fund Facility (EFF) for Pakistan, a $7 billion bailout aimed at averting default. While this package, that kicked in from Sept 2024, provides short-term liquidity, critics argue that repeated IMF programs since the 1980s have fostered a cycle of dependency, with austerity measures often exacerbating public discontent. For instance, subsidy cuts and tax hikes under previous IMF agreements have triggered protests, highlighting the tension between fiscal discipline and social stability.

Structural taxation weaknesses persist: the tax-to-GDP ratio remains a meagre 8.77% [4] (compared to 11.7 % [5] In India and around 40 % per cent in Europe [6]), hindered by evasion and a narrow tax base, while loss-making state-owned enterprises drain billions annually. Additionally, climate change has devastated agriculturecontributing 23% to GDP [7]through floods and droughts, displacing communities and disrupting supply chains. Human capital development lags, with literacy rates stagnant at 62% [7] and vocational training inadequate to meet labour market demands, fueling a brain drain as skilled workers emigrate.

The IMF’s recent downgrade of Pakistan’s 2025 GDP growth forecast from 3.2% to 3% [8] reflects skepticism about reform implementation. Sustainable recovery hinges on systemic changes: broadening tax reforms, privatizing inefficient industries, combating corruption, and investing in education and technology. Without such measures, Pakistan risks entrenching a “beg-and-borrow” economy, jeopardizing sovereignty and long-term resilience. Lessons from India and from nations like Indonesia and Egyptwhich combined IMF support with homegrown reforms to stabilize economiesoffer a potential roadmap. Achieving this requires systemic overhaul: political consensus, security enhancements, and a commitment to equitable growth to ensure sustainable transformation is prioritized over short-term relief. Most importantly, it requires removing the structural anomaly of ‘Military Inc’, an army deeply entrenched in the economy, triggering inefficiencies and blocking reform.

How the IMF’s Extended Fund Facility Has Fostered Dependency

The Extended Fund Facility (EFF), established by the International Monetary Fund (IMF) in 1974, was designed to address the unique economic challenges faced by countries grappling with chronic structural weaknesses and protracted balance of payments (BoP) crisesprecisely the issues plaguing Pakistan today. Created in the wake of the 1970s global oil shocks and inflationary pressures, the EFF emerged as a response to the limitations of the IMF’s traditional short-term lending instruments, such as Stand-By Arrangements (SBAs), which were ill-suited for nations requiring deeper, longer-term reforms. Unlike SBAs, which typically span 12–24 months and focus on immediate liquidity needs, the EFF allows for extended engagement, with repayment periods ranging from 4.5 to 10 years [9]. This longer horizon was meant to provide breathing room for governments to implement structural reformssuch as overhauling tax systems, privatizing state-owned enterprises, or modernizing infrastructurethat may take years to yield tangible economic benefits [9].

Countries eligible for the EFF, like Pakistan, often suffer from chronic structural impediments, including rigid fiscal frameworks, inefficient public sectors, energy shortages, and low export diversification. These issues contribute to persistent BoP deficits, where a nation’s imports and debt repayments consistently outstrip its export earnings and foreign exchange reserves. For instance, Pakistan’s BoP crisis is exacerbated by its reliance on costly energy imports, a narrow tax base (with a tax-to-GDP ratio of just 8.77% [4]), and stagnant export sectors like textiles, which face competition from regional rivals. The EFF’s extended timeline aims to break this cycle by enabling reforms such as broadening the tax base, reducing energy subsidies, and improving governancemeasures that require political stamina and time to gain public acceptance.

Pakistan’s history with the EFF illustrates both its potential and pitfalls: with the 2024 EFF, the country has availed twenty-five IMF programs, since 1958, including EFF arrangements. Many reform programs stalled due to political resistance or external shocks (e.g., floods, pandemics). The 2019 EFF, a $6 billion package, demanded politically tough reforms like hiking energy prices and increasing tax revenues, but compliance wavered amid inflationary backlash and governance gaps [10].

Critics argue that the EFF’s success hinges on domestic political will and institutional capacityfactors often in short supply in crisis-hit nations. While Indonesia’s post-1997 EFF program stabilized its economy through banking reforms and deregulation [11], Pakistan’s repeated reliance on the facility underscores a cycle of dependency, with short-term gains overshadowed by unmet structural benchmarks. Nevertheless, the EFF remains a critical lifeline for countries like Pakistan, offering not just financing but a framework for credibility with international lenders. The challenge lies in ensuring that borrowed time translates into sustainable change, rather than perpetuating a pattern of crisis and rescue.

IMF Lending Data to Pakistan from 1958 to2024

Note: The amount in this table is in SDR (Special Drawing Rights) value: The currency value of the SDR is determined by summing the values in U.S. dollars, based on market exchange rates, of a basket of major currencies (the U.S. dollar, Euro, Japanese yen, pound sterling and the Chinese renminbi). The SDR currency value is calculated daily except on IMF holidays, or whenever the IMF is closed for business, or on an ad-hoc basis to facilitate unscheduled IMF operations. The SDR valuation basket is reviewed and adjusted every five years.

| Sr No | Facility | Date of Arrangement | Expiration Date | Amount Agreed | Amount Drawn | Amount Outstanding |

| 1 | Extended Fund Facility | Sep 25, 2024 | Oct 24, 2027 | 53,20,000 | 7,60,000 | 7,60,000 |

| 2 | Standby Arrangement | Jul 12, 2023 | Apr 29, 2024 | 22,50,000 | 22,50,000 | 22,50,000 |

| 3 | Extended Fund Facility | Jul 03, 2019 | Jun 30, 2023 | 49,88,000 | 30,38,000 | 28,91,333 |

| 4 | Rapid Financing Instrument | Apr 16, 2020 | Apr 20, 2020 | 10,15,500 | 10,15,500 | 2,53,875 |

| 5 | Extended Fund Facility | Sep 04, 2013 | Sep 30, 2016 | 43,93,000 | 43,93,000 | 5,34,333 |

| 6 | Standby Arrangement | Nov 24, 2008 | Sep 30, 2011 | 72,35,900 | 49,36,035 | 0 |

| 7 | Extended Credit Facility | Dec 06, 2001 | Dec 05, 2004 | 10,33,700 | 8,61,420 | 0 |

| 8 | Standby Arrangement | Nov 29, 2000 | Sep 30, 2001 | 4,65,000 | 4,65,000 | 0 |

| 9 | Extended Fund Facility | Oct 20, 1997 | Oct 19, 2000 | 4,54,920 | 1,13,740 | 0 |

| 10 | Standby Arrangement | Dec 13, 1995 | Sep 30, 1997 | 5,62,590 | 2,94,690 | 0 |

| 11 | Extended Credit Facility | Feb 22, 1994 | Dec 13, 1995 | 6,06,600 | 1,72,200 | 0 |

| 12 | Extended Fund Facility | Feb 22, 1994 | Dec 04, 1995 | 3,79,100 | 1,23,200 | 0 |

| 13 | Standby Arrangement | Sep 16, 1993 | Feb 22, 1994 | 2,65,400 | 88,000 | 0 |

| 14 | Structural Adjustment Facility Commitment | Dec 28, 1988 | Dec 27, 1991 | 3,82,410 | 3,82,410 | 0 |

| 15 | Standby Arrangement | Dec 28, 1988 | Nov 30, 1990 | 2,73,150 | 1,94,480 | 0 |

| 16 | Extended Fund Facility | Dec 02, 1981 | Nov 23, 1983 | 9,19,000 | 7,30,000 | 0 |

| 17 | Extended Fund Facility | Nov 24, 1980 | Dec 01, 1981 | 12,68,000 | 3,49,000 | 0 |

| 18 | Standby Arrangement | Mar 09, 1977 | Mar 08, 1978 | 80,000 | 80,000 | 0 |

| 19 | Standby Arrangement | Nov 11, 1974 | Nov 10, 1975 | 75,000 | 75,000 | 0 |

| 20 | Standby Arrangement | Aug 11, 1973 | Aug 10, 1974 | 75,000 | 75,000 | 0 |

| 21 | Standby Arrangement | May 18, 1972 | May 17, 1973 | 1,00,000 | 84,000 | 0 |

| 22 | Standby Arrangement | Oct 17, 1968 | Oct 16, 1969 | 75,000 | 75,000 | 0 |

| 23 | Standby Arrangement | Mar 16, 1965 | Mar 15, 1966 | 37,500 | 37,500 | 0 |

| 24 | Standby Arrangement | Dec 08, 1958 | Sep 22, 1959 | 25,000 | 0 | 0 |

Table 1 Source: IMF [12]

The 2013 IMF Extended Fund Facility (EFF) to Pakistan

In September 2013, Pakistan secured a three-year, $6.6 billion Extended Fund Facility (EFF) from the IMF to address a dire economic crisis [13]. At the time, the country faced plummeting foreign reserves (down to $3.2 billion [14], covering just three weeks of imports), a fiscal deficit exceeding 8% of GDP [13], chronic energy shortages fueled by $5 billion in circular debt, the unpaid financial shortfall in Pakistan’s energy sector, causing cash flow disruptions across the supply chain.) and sluggish GDP growth of 3.7%. [15]. The program aimed to stabilize the economy through fiscal consolidation, structural reforms, and restoring investor confidence. Key components included reducing the fiscal deficit to 3.5% of GDP by 2016 [13], broadening the tax base, eliminating energy subsidies, privatizing loss-making state-owned enterprises (SOEs), and transitioning to a market-driven exchange rate. Structural benchmarks included overhauling tax administration, introducing a VAT-style sales tax, and strengthening social safety nets to cushion austerity impacts.

The 2013 Extended Fund Facility (EFF) from the IMF was granted to Pakistan in the context of a relatively stable political transition following the first democratic transfer of power after the Musharraf era. The general elections in May 2013 were considered relatively free and competitive, leading to Nawaz Sharif’s Pakistan Muslim League-Nawaz (PML-N) forming the government. This political stability, along with the commitment to economic reforms, created a favourable environment for securing the $6.6 billion IMF bailout to address Pakistan’s economic crisis, including dwindling foreign reserves, a high fiscal deficit, and chronic energy shortages.

However, despite initial progress, Pakistan’s implementation of the program was inconsistent and politically compromised. Tax reforms, a cornerstone of the EFF, faltered due to elite resistance. The government avoided taxing politically sensitive sectors like agriculture and real estate, which contributed 23% [7] and 2.8 % [16] respectively to GDP but only 0.6% (agriculture, 2017-18) [17] and 0.003 % (real estate, 2020-21 ) [18] to tax revenues, and instead relied on regressive indirect taxes that burdened the poor. Efforts to modernize the Federal Board of Revenue (FBR) were undermined by corruption and inefficiency, failing to reach the 13% tax to GDP [19] target. Energy reforms also stalled. Though electricity tariffs were raised public backlash and pre-election populism forced the government to delay further hikes. Privatisation of SOEs like Pakistan International Airlines (PIA) and power distribution companies collapsed due to union strikes and political opposition [20].

Structural reforms, such as the proposed VAT-style RGST, were abandoned amid opposition from traders and provinces. Loss-making SOEs continued to drain $4 billion annually in subsidies, while external shockslike the 2014–2015 global oil price crash and the costs of counterterrorism operations (e.g., Zarb-e-Azb)diverted attention and resources from reform agendas.

By the program’s conclusion in 2016 (extended to 2018), Pakistan achieved superficial stability: foreign reserves rebounded to $18 billion [21], aided by IMF inflows and Chinese CPEC investments, and GDP growth rose to 5.5% in 2017 [22]. However, these gains masked unresolved structural flaws. Tax evasion, energy inefficiencies, and public debt (72% of GDP by 2018 [23] worsened, setting the stage for a renewed crisis by 2018, which necessitated another IMF bailout in 2019. The 2013 EFF’s failure underscored a recurring pattern: short-term compliance with IMF conditions without confronting vested interestsfeudal elites, energy unions, or the military-industrial complexyielded temporary relief but entrenched long-term fragility. The episode highlighted how political unwillingness to prioritize systemic reform over populist concessions perpetuates a cycle of dependency, rendering IMF programs Band-Aid solutions rather than catalysts for sustainable transformation. Taimur Rahman, a political economist teaching at the Lahore University of Management Science, blamed the ruling classes for these dismal conditions and drew a comparison between India and Pakistan: “The ruling class of Pakistan, unlike their Indian counterparts, have always splurged on luxury products and the military” [24].

The 2019 IMF Extended Fund Facility (EFF) to Pakistan

In July 2019, Pakistan entered a 39-month, $6 billion Extended Fund Facility (EFF) with the IMF, marking its 22nd program since 1958. The agreement came amid a deepening economic crisis: foreign reserves had dwindled to $7.2 billion (covering less than two months of imports) [25], the budget deficit stood at 8.9% of GDP [26], and public debt soared to 84% of GDP [27], The PTI government, led by Prime Minister Imran Khan, sought the EFF to avert a balance-of-payments crisis, stabilize the rupee and restore investor confidence. While the 2019 EFF shared core objectives with the 2013 programfiscal consolidation, tax reforms, and energy sector overhaulsit diverged in its emphasis on social spending, anti-corruption measures, and adjustments for external shocks like COVID-19 [10]. However, similar structural challenges and political constraints undermined its implementation.

This happened in the political context of the same-page hybrid government with army chief Bajwa and a new ‘same-page’ Prime Minister, Imran Khan, who took over after the elections in 2018. Despite the advice to go into an IMF program, he initially resisted, trying to tap the largesse of friendly governments like Saudi Arabia and China. He eventually succumbed and bowed to the tradition of new civilian governments rushing to the IMF to stabilise their regimes.

According to the 2019 IMF EFF package had five key components. First, fiscal consolidation aimed to reduce the fiscal deficit to 2.4% of GDP by 2023 through austerity measures, including subsidy cuts, tax revenue increases, and reductions in development spending. The program sought to expand the tax-to-GDP ratio by broadening the tax base, eliminating exemptions, and cracking down on evasion. Second, monetary and exchange rate reforms mandated a shift to a market-determined exchange rate, ending the State Bank of Pakistan’s (SBP) interventions to stabilize the rupee. Monetary policy was tightened to curb inflation while granting the SBP greater autonomy to target inflation. Third, energy sector overhauls targeted Pakistan’s chronic circular debt, which had surged to $17.5 billion by 2019 [28]. The program mandated electricity tariff hikes, reductions in transmission losses, and restructuring of power-sector contracts. Subsidies for electricity and gas were to be phased out, particularly for non-residential consumers. Fourth, structural reforms included the privatisation or restructuring of loss-making state-owned enterprises (SOEs) such as Pakistan Steel Mills and PIA. The government also pledged to strengthen governance through anti-corruption initiatives, including digitizing procurement and enhancing transparency in public-sector projects.

Finally, the EFF expanded the Ehsaas Program, Pakistan’s social safety net, to mitigate the impact of austerity on low-income households. The 2019 EFF bore several similarities to the 2013 program. Both focused on fiscal and tax reforms, prioritizing subsidy reductions and tax base expansion, though resistance from elites remained a common obstacle. Agriculture and real estatecontributing 23% [7] and 2.8% to GDP [16], respectivelyremained undertaxed, while indirect taxes such as sales tax hikes and petroleum levies disproportionately burdened lower-income groups. The energy sector challenges persisted, with circular debt rising despite tariff hikes. Privatisation of power distribution companies (DISCOs) was planned but met with significant political resistance and public protests, leading to delays [29]. Similarly, SOE privatisation gridlock hindered reforms, as the PTI government faced strikes from PIA employees and legal challenges, mirroring the difficulties faced by the PML-N administration in 2013. Additionally, external shocks disrupted the programs. While the 2013 EFF dealt with oil price volatility and military expenditures from Operation Zarb-e-Azb, the 2019 program was severely impacted by the COVID-19 pandemic.

Despite these similarities, the 2019 EFF also introduced some new elements. One major shift was the program’s social spending focus, with the Ehsaas Program expanded to cover 12 million families, up from 5.3 million under the Benazir Income Support Program (BISP) in 2013 [10]. The government also introduced emergency cash transfers during COVID-19 to support vulnerable populations. Another distinction was the anti-corruption agenda, which saw reforms tied to digitizing tax filings, public procurement, and asset declarations for officials. However, these measures faced bureaucratic pushback and limited enforcement. Additionally, the monetary policy autonomy aspect of the 2019 program was unprecedented. Legislative amendments were introduced to grant the SBP operational independencea structural shift absent in 2013. Critics argued that this prioritisation of inflation control over growth worsened unemployment. The China-Pakistan Economic Corridor (CPEC) debt also distinguished the 2019 program from its predecessor. With repayments to Chinese power plants adding to circular debt, the IMF urged transparency in CPEC contracts, but disclosures remained minimal.

Finally, this EFF faced major challenges due to political instability in Pakistan. In early April 2022, the program hit a deadlock when then-Prime Minister Imran Khan announced a relief package that included tax amnesty schemes and energy price cuts, which were seen as reversals of previously agreed reforms with the IMF [30].

The PTI government’s collapse in April 2022, amid political turmoil, further derailed the reform agenda. By 2023, Pakistan once again faced balance-of-payments pressures, forcing the new PDM coalition to seek another IMF bailout.

The 2024 IMF Extended Fund Facility (EFF) to Pakistan

The 2024 Extended Fund Facility (EFF) for Pakistan is a 37-month program approved by the International Monetary Fund (IMF) to support Pakistan’s efforts in tackling economic challenges, strengthening resilience, and fostering sustainable growth. The program built on the macroeconomic stability achieved over the past year and focuses on strengthening public finances, reducing inflation, rebuilding external buffers, and eliminating economic distortions to promote private sector-led growth.

According to the IMF Country Report 24/310, One of the core priorities of the 2024 EFF was macroeconomic sustainability, which involved enhancing policy-making credibility through consistent fiscal, monetary, and exchange rate policies [31]. The program also emphasized improving public spending efficiency and raising fairer and more effective taxation, particularly by targeting under-taxed sectors. Another key focus area is productivity and competitiveness, which sought to improve Pakistan’s business environment by eliminating state-created distortions, increasing competition, streamlining subsidies, improving the foreign direct investment (FDI) framework, strengthening banking intermediation, and investing in human capital.

The program also prioritized state-owned enterprise (SOE) and public service reforms, aiming to improve SOE governance through restructuring and privatisation. It also sought to reduce inefficiencies in the energy sector by addressing cost structures and gradually phasing out government intervention in price setting. Additionally, the 2024 EFF had a strong emphasis on climate resilience, supporting the implementation of Pakistan’s C-PIMA Action Plan and its National Adaptation Plan to tackle environmental challenges [31].

To qualify for the EFF funding, Pakistan had to undertake several policy measures, including significant tax reforms to broaden the tax base. The government also had to increase electricity prices and generate more revenue from non-tax sources, such as petroleum levies and electricity tariffs. Additionally, fiscal measures were introduced to maintain a balance between federal and provincial government spending, imposing taxes on the agricultural sector and prohibiting new subsidies.

Like previous IMF bailout programs, the 2024 EFF focused on addressing Pakistan’s balance of payments issues and implementing long-term structural reforms. The program demands strict policy measures that, while necessary for economic stability, were viewed as harsh by some experts. Key elements such as fiscal consolidation, monetary policy adjustments, energy sector reforms, and SOE restructuring are also consistent with previous IMF programs for Pakistan.

A key distinction of the 2024 EFF is its strong focus on climate resilience, which was not as prominent in earlier IMF packages. Additionally, this program is designed to align with the new government’s broader reform agenda, emphasizing inclusive and long-term economic growth. Another major difference is that the 2024 EFF is integrated with Pakistan’s Thirteenth Five-Year Plan (2024–2029), which introduces the 5E Frameworkfocusing on Exports, E-Pakistan (digital economy), Energy & Infrastructure, Environment & Climate Change, and Equity & Empowerment [31] [32]. This broader framework sets a more strategic direction for Pakistan’s economic recovery beyond immediate stabilisation measures.

Overall, while the 2024 EFF shares similarities with previous IMF programs in its emphasis on economic stabilisation, fiscal discipline, and structural reforms, its distinct focus on climate resilience, digital economy, and inclusive growth reflects a more modernized approach to addressing Pakistan’s long-term economic challenges [31].

Perpetual Economic Problems of Pakistan

Pakistan’s economic crisis is rooted in four perpetual causes: weak economic structure, failed land reforms, military influence in the economy and politics, and low foreign direct investment (FDI). The country’s economic foundation remains fragile due to a narrow industrial base, an inefficient taxation system, and a reliance on imports over exports, leading to persistent trade deficits. Failed land reforms have resulted in feudal dominance, preventing equitable wealth distribution and hindering agricultural productivity. The military’s deep involvement in both economic and political affairs has led to resource misallocation, weakened civilian institutions, and deterred investor confidence. It led to extreme elite capture of Pakistan’s institutions the 1950s which became another impediment to reform. Additionally, low FDI, driven by political instability, security concerns, and inconsistent policies, has stifled economic growth and technological advancement. Each of these factors provided unique headwinds to economic expansion, as elaborated below.

Weak Economic Structure

Pakistan’s perpetual economic crisis is rooted in its weak economic structure, which manifests through several critical issues, including low tax revenue, high external debt, and inefficiencies in the energy sector. These structural weaknesses create a vicious cycle of low growth, fiscal deficits, and economic instability, preventing the country from achieving sustainable development.

- Weak Tax Revenue and Resource Mobilisation

One of the fundamental causes of Pakistan’s economic crisis is its chronically low tax revenue, which accounts for less than 10% of GDP [4] a stark contrast to the OECD average of around 34% [33]. This low tax collection is a result of widespread tax evasion, weak enforcement mechanisms, a narrow tax base, and a reliance on indirect taxation rather than progressive direct taxation. Large segments of the economy, including agriculture, retail, and informal businesses, remain under-taxed or entirely outside the tax net, leading to a severe shortfall in government revenues.

The consequences of this weak tax system are profound. With limited fiscal resources, the government struggles to invest in critical public services such as education, healthcare, and infrastructure. This underinvestment further exacerbates poverty, income inequality, and low productivity, hindering long-term economic growth. Additionally, inadequate tax revenue forces the government to rely on deficit financing and external borrowing, leading to a continuous rise in national debt. Without substantial reforms to broaden the tax base and improve compliance, Pakistan’s ability to fund development projects and stabilize its economy remains severely constrained.

- High External Debt and Dependency

Pakistan’s heavy reliance on external borrowing has created a debt trap that threatens long-term economic stability. According to Trading economics the country’s external debt currently stands at approximately $131 billion [34], and debt servicing consumes a significant portion of the national budget, leaving little fiscal space for developmental spending. A major issue is that Pakistan often borrows to repay existing debt rather than investing in productive sectors, leading to a cycle of dependency on international lenders, including the International Monetary Fund (IMF), World Bank, and bilateral creditors such as China and Gulf nations.

Repeated IMF bailout programs highlight the government’s failure to implement necessary structural reforms, such as broadening the tax base, improving public sector efficiency, and reducing fiscal deficits. Instead of long-term solutions, policymakers resort to short-term rollovers, austerity measures, and new loans, which further constrain economic growth and increase social unrest. The depreciation of the Pakistani Rupee, coupled with rising global interest rates, has worsened debt servicing costs, making it even more difficult for Pakistan to break free from this financial cycle.

- Energy Sector Inefficiencies

Pakistan’s energy sector is one of the most inefficient and poorly managed sectors of the economy, posing a major obstacle to industrial growth and economic stability. The country faces frequent power shortages, unreliable electricity supply, and a heavy reliance on imported fossil fuels, which exposes it to global price volatility. Currently, energy imports account for a significant share of Pakistan’s trade deficit, increasing inflationary pressures and reducing the competitiveness of local industries.

The energy crisis is further exacerbated by poor governance, circular debt, and outdated infrastructure. The circular debt problem, where power producers are unable to recover costs from distributors due to high transmission losses and unpaid bills, has reached alarming levels, exceeding 2.8 trillion PKR ($10 billion) [35]. This financial strain forces the government to subsidize electricity prices, adding to fiscal deficits and diverting resources from essential development projects.

Moreover, despite having vast renewable energy potential, including solar, wind, and hydropower, Pakistan has failed to diversify its energy mix due to a lack of investment and policy incentives. According to Institute for Energy Economics and Financial Analysis, Dependence on imported liquefied natural gas (LNG) and furnace oil has made the energy sector highly vulnerable to external shocks, affecting businesses, inflation, and overall economic productivity [36].

Failed Land Reforms

The history of land reforms in Pakistan reflects a persistent struggle between economic equity and entrenched feudal power, shaping the country’s socio-economic landscape over decades. Land ownership has long been concentrated in the hands of a small elite, creating stark economic inequalities and limiting opportunities for the broader rural population. Recognizing this issue, successive governments attempted to introduce land reforms to break feudal control, promote equitable wealth distribution, and enhance agricultural productivity. However, these efforts largely failed due to legal loopholes, elite resistance, and weak enforcement, leading to continued economic disparity and underdevelopment.

While India had rolled out democratic elections from 1951 and land reforms from, the first weak attempt at land reform In Pakistan came in 1959 under dictator Ayub Khan, who sought to limit landlord dominance by imposing a ceiling of 500 acres for irrigated land and 1,000 acres for unirrigated land [37]. The objective was to redistribute surplus land among landless farmers and weaken the power of the feudal class that had historically controlled agricultural production and rural labour. However, the implementation of these reforms was flawed. Large landowners exploited legal loopholes, transferring land to family members or establishing fake cooperative farms to evade ceilings. As a result, the intended redistribution remained minimal, and the entrenched economic disparities persisted. While Ayub’s reforms introduced a legal framework for land ownership regulation, they failed to bring about substantial structural change.

A more ambitious effort was undertaken in 1972 by Prime Minister Zulfiqar Ali Bhutto, leader of the socialist PPP, who sought to push the boundaries of land redistribution further. His reforms lowered land ceilings to 100 acres for irrigated land and 200 acres for unirrigated land, a drastic reduction aimed at dismantling feudal control over rural Pakistan [38]. However, despite the progressive rhetoric surrounding these measures, their execution was hampered by corruption and political favouritism. Many influential landlords, often with strong political connections, managed to bypass the restrictions through bureaucratic manipulations and forged land records. Instead of empowering small farmers, these reforms primarily served to consolidate the power of the ruling class while providing only a symbolic gesture towards land equity. Consequently, rural feudal structures remained intact, and the economic benefits of land redistribution failed to materialize for the majority of landless peasants.

The final major land reform initiative occurred in 1977, also under Bhutto, in an attempt to further curtail large landholdings and empower small farmers [38]. However, these efforts faced fierce resistance from landlords, many of whom held significant political influence. The situation worsened after Bhutto’s removal from power, as the new military-led government and judiciary reversed many of the reforms. Courts ruled that the measures were unconstitutional or un-Islamic, effectively restoring the privileges of the landed elite. This not only reinforced the feudal status quo but also created long-term uncertainty in agricultural investment, as frequent legal reversals discouraged structural improvements and modernisation in the sector.

The failure to effectively implement land reforms has had profound and lasting consequences on Pakistan’s economy and society. One of the most significant impacts has been the continued concentration of wealth among a small elite, which has hindered overall economic growth and deepened rural poverty. With much of the land still controlled by a few powerful families, opportunities for upward mobility remain scarce for the majority of Pakistan’s rural population. This economic divide has exacerbated social inequalities, limiting access to education, healthcare, and economic opportunities for those in lower socio-economic strata.

Additionally, the persistence of small-scale, fragmented farms has contributed to agricultural inefficiency. Many small farmers lack the resources, technology, and access to credit necessary to enhance productivity, resulting in suboptimal yields and stagnation in the agricultural sector. Given that agriculture is a vital component of Pakistan’s economy, its inefficiency has broader implications for food security, rural employment, and overall economic development. The lack of large-scale agricultural modernisation has also meant that Pakistan struggles to compete with other nations in agricultural exports, limiting foreign exchange earnings and economic resilience.

These factors collectively contribute to Pakistan’s broader economic crisis. The lack of land reform has not only stifled equitable economic growth but also discouraged investment in both agriculture and other sectors due to political instability and economic uncertainty. Without addressing the structural issues embedded in land ownership, efforts to promote sustainable economic development and poverty alleviation will remain limited. Moving forward, any meaningful attempt to tackle Pakistan’s economic challenges must involve revisiting land reform policies with a commitment to genuine implementation, ensuring fair land distribution, and fostering an environment conducive to agricultural innovation and rural prosperity.

The Security State Drives Pakistan’s Economic Woes

Pakistan’s ongoing economic crisis is deeply intertwined with the military’s overwhelming influence over state affairs. The Pakistan Army, historically a dominant force in the country’s political and economic landscape, has contributed significantly to the misallocation of resources, control over key economic sectors, and persistent political instability. These factors collectively hinder economic progress, exacerbate financial mismanagement, and limit the country’s ability to implement meaningful reforms.

Most glaring is the misallocation of resources, with Pakistan’s military budget continuing to grow even in the face of a severe economic crisis. Despite rising inflation, increasing debt, and dwindling foreign reserves, the defence budget hiked by approximately 15% (3.6 % of GDP) in 2024-25, published in a report by Business Standard [39], further diverting funds from critical sectors such as education, healthcare, and infrastructure. This excessive spending on defense not only limits investments in human capital but also curtails social welfare initiatives, exacerbating poverty and slowing economic growth. Countries that have successfully developed strong economies have prioritized human development, innovation, and industryareas where Pakistan continues to lag due to its disproportionate focus on military expenditure.

Beyond budgetary concerns, the Pakistan Army’s direct control over economic assets has created a parallel economy that fosters inefficiencies and stifles private sector growth. The military owns vast tracts of real estate, dominates large-scale agricultural production, and operates an extensive network of businesses under military-run conglomerates such as the Fauji Foundation, Army Welfare Trust, and Bahria Foundation. These enterprises of ‘Military Inc.’ enjoy preferential treatment, including tax exemptions and regulatory leniency, which distort market competition and discourage private sector participation. The military’s dominance in key industriesranging from construction to telecommunicationsrestricts economic dynamism and innovation, as private businesses struggle to compete with state-backed military enterprises. Moreover, the lack of transparency in military-controlled economic activities makes it difficult to implement fiscal reforms, as the military’s financial dealings are largely exempt from civilian oversight. This opaque economic system not only limits government revenue but also fosters corruption and rent-seeking behaviour, further weakening Pakistan’s financial stability.

Perhaps the most damaging impact of military dominance is its interference in political affairs, which has perpetuated instability and policy inconsistencytwo critical factors that deter investment and economic growth. Over the years, the military’s influence over civilian governments has led to repeated political upheavals, weakening democratic institutions and preventing the formulation of long-term economic strategies. Military-backed interventions, including frequent government overthrows and engineered political transitions, have resulted in inconsistent economic policies, discouraging both domestic and foreign investors. This instability has contributed to high inflation, increasing public debt, and fiscal mismanagement, as successive governments struggle to implement coherent economic plans. Additionally, the military’s direct and indirect control over key policy decisions often obstructs necessary economic reforms, such as taxation restructuring and privatisation of inefficient state-owned enterprises.

The consequences of military overreach extend to Pakistan’s relations with international financial institutions and donor agencies. Global lenders, including the International Monetary Fund (IMF) and the World Bank, often demand structural economic reforms and fiscal discipline as conditions for financial assistance. However, the military’s deep entrenchment in the economy, along with its resistance to transparency and accountability, complicates efforts to meet these conditions. The lack of trust in Pakistan’s ability to implement reforms has made it difficult to secure long-term financial aid, forcing the country into repeated cycles of economic bailouts. Additionally, the perception of military dominance discourages foreign direct investment (FDI), as businesses fear unpredictable policy shifts, excessive bureaucracy, and regulatory hurdles that favour military-affiliated enterprises over private-sector growth.

Furthermore, Ayesha Siddiqa examines the extensive involvement of Pakistan’s military in commercial enterprises and how this “Milbus” (military business) affects the nation’s economy and democratic processes. She argues that the military’s economic autonomy fosters a predatory political style, hindering democratic development and economic transparency [40].

While Shahrukh Rafi Khan, Aasim Sajjad Akhtar, and Sohaib Bodla: In “The Military and Denied Development in the Pakistani Punjab,” discuss how the military’s dominance in Pakistan has led to economic underdevelopment in certain regions. They highlight the military’s accumulation of power through economic ventures and its impact on civilian oversight and democratic sustainability [41].

In sum, Pakistan’s economic crisis cannot be addressed without confronting the military’s outsized role in financial and political decision-making. The unchecked expansion of defence budgets at the cost of essential public services, the monopolisation of key economic sectors, and persistent political interference have all contributed to economic stagnation.

Low FDI as a Key Factor in Pakistan’s Economic Crisis

Foreign Direct Investment (FDI) plays a crucial role in economic growth by providing capital, fostering technological advancements, creating employment opportunities, and stabilizing foreign exchange reserves. However, Pakistan has faced a significant decline in FDI inflows, contributing to its ongoing economic crisis. Several factors, including political instability, security concerns, and inconsistent policies, have driven away potential investors, leading to stagnation and financial vulnerability. One of the primary consequences of low FDI is declining investment which has substantially reduced capital formation and industrial growth. Pakistan’s inability to attract foreign investors has limited access to advanced technology, reduced job creation, and hindered economic expansion. The lack of investment in key sectors, such as manufacturing, energy, and infrastructure, has stifled productivity and innovation, causing economic stagnation. This, in turn, has contributed to rising unemployment, decreased economic opportunities, and increased reliance on external borrowing to cover fiscal deficits.

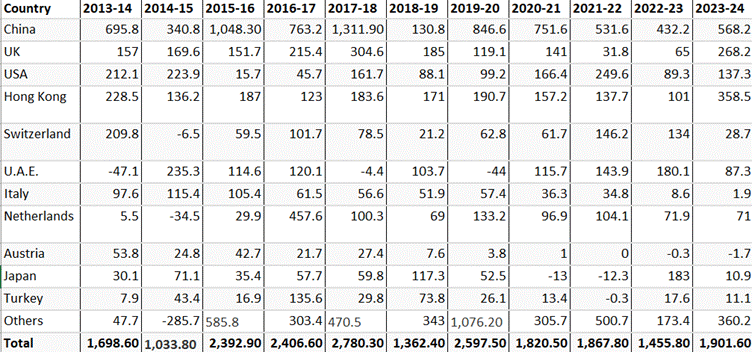

Country Wise Net FDI in Pakistan ($ Million)

Figure 1 Source: Pakistan Board of Investment [42]

The above Table shows that China has been the backbone of Pakistan’s foreign direct investment (FDI) inflows over the past decade, consistently outpacing all other countries. Since the launch of the China-Pakistan Economic Corridor (CPEC) in 2015, Chinese investments have surged, to over $1 billion in 2015-16 and continuing to dominate in subsequent years with a peak of $1.3 billion in 2017-18. Even as global interest in Pakistan’s economy fluctuated, China remained a steadfast investor, contributing $568.2 million in 2023-24more than double the FDI from the UK, the second-largest contributor. Without Chinese capital, Pakistan’s FDI inflows would be significantly weaker, highlighting the country’s heavy reliance on Beijing for infrastructure, energy, and industrial investments.

If China’s strategic investments are removed from this mix, the picture looks even more pessimistic. Geopolitically, at least from 2021 after US withdraw from Afghanistan in 2021, Pakistan’s ‘geostrategic rents’, based on leveraging its strategic location, have dried up. Apart from the Chinese, most of the global investors would look for economic rather than strategic returns.

The impact on economic stability has been profound, as dwindling FDI inflows have left Pakistan highly vulnerable to external shocks. The country’s foreign exchange reserves are critically low, making it difficult to maintain exchange rate stability and meet international financial obligations. A persistent balance of payments crisis has increased reliance on short-term loans and financial bailouts from institutions like the International Monetary Fund (IMF), further exacerbating economic uncertainty. The depreciation of the Pakistani Rupee, driven by a lack of foreign investment and capital inflows, has led to inflationary pressures, making essential goods and services more expensive for the average citizen.

A major factor behind low FDI inflows is the loss of investor confidence, which has been exacerbated by political instability and security threats. Pakistan’s political landscape has been marred by frequent leadership changes, weak governance, and policy inconsistencies, deterring long-term investment commitments. Investors seek a stable and predictable business environment, yet Pakistan’s history of abrupt policy shifts and regulatory uncertainty has made it an unattractive destination. Additionally, the persistent threat of terrorism and regional security challenges has further discouraged foreign businesses from entering or expanding their operations in the country.

Sadia Bano, Yuhuan Zhao, Ashfaq Ahmad, Song Wang, and Ya Liu: In their study titled “Why Did FDI Inflows of Pakistan Decline? From the Perspective of Terrorism, Energy Shortage, Financial Instability, and Political Instability”, analyze factors contributing to the decline of FDI inflows into Pakistan. They identify terrorism, energy shortages, financial instability, and political instability as significant deterrents to foreign investment, which, in turn, exacerbate the country’s economic problems [43].

The low levels of FDI have also created a vicious cycle in which economic stagnation fuels political instability, which in turn discourages further investment. Without sufficient foreign capital, Pakistan struggles to develop its infrastructure, modernize industries, and enhance productivity, leaving it increasingly dependent on external financial aid. The inability to generate sustainable economic growth through investment-driven initiatives has contributed to a prolonged financial crisis, limiting the government’s capacity to implement long-term economic reforms.

To address these challenges, Pakistan needs to take urgent steps to restore investor confidence and attract FDI. This includes the tall order of ensuring political stability, implementing investor-friendly policies, enhancing security measures, and promoting transparency in economic decision-making. Strengthening legal protections for investors, improving ease of doing business, and offering tax incentives would be critical to encourage multinational corporations and foreign firms to invest in Pakistan’s key industries. Additionally, fostering regional trade relations and signing bilateral investment agreements could help integrate Pakistan into global supply chains, enhancing its appeal as an investment destination. All these policies seem foreign to a security state’s imagination.

Conclusion: A Worsening Crisis

Pakistan’s “Decade of Decadence” (2013–2024) stands as a stark testament to the consequences of systemic neglect, political short-sightedness, and entrenched power structures. Over these years, the economy spiralled under the weight of chronic structural flaws: a collapsing rupee, inflationary surges, and stagnant growth exposed the fragility of a system reliant on borrowed time and IMF bailouts. Repeated cycles of crisis and rescuethrough Extended Fund Facilities in 2013, 2019, and 2024have highlighted a pattern of superficial compliance with reform mandates, undermined by elite capture, military dominance, and a lack of political will. While these programs provided temporary liquidity, they failed to address the root causes of Pakistan’s economic malaiseweak tax systems, energy sector decay, feudal agrarian structures and an outsized capture of the economy by Military Inc.leaving the country trapped in a vortex of debt and dependency.

The military’s stranglehold over politics and the economy has driven this decline through multiple pathways. By prioritizing defence spending over human capital, monopolizing key industries, and destabilizing governance, the military-industrial complex stifled innovation, discouraged investment, and diverted resources from critical public services. Similarly, the failure of land reforms cemented rural inequality, perpetuating agricultural inefficiency and social unrest. Meanwhile, plummeting FDI reflected eroding investor confidence, driven by political volatility, security risks, and regulatory unpredictability.

Yet, amid this bleak landscape, Pakistan’s government tries to talk up a few positives. The 2024 EFF’s emphasis on climate resilience, digital transformation, and inclusive growth is said to signal a shift toward modernizing reforms. Lessons from nations like Indonesia and Egypt demonstrate that IMF-backed stabilisation, paired with homegrown structural overhauls, could potentially yield sustainable recovery. But the rhetoric is not backed by sustained action. Pakistan’s path forward demands more than technocratic adjustmentsit requires dismantling the vested interests that perpetuate inequality and inefficiency. This includes taxing untapped sectors like agriculture and real estate, privatizing loss-making SOEs, and empowering institutions free from military or feudal influence.

Ultimately, Pakistan’s future hinges on its ability to confront hard truths: economic sovereignty cannot coexist with elite impunity, nor can stability thrive amidst institutionalized inequity. Breaking free from this decade of dependence on the IMF and quick fixes will demand courage, transparency, and a collective commitment to prioritizing people over power. Without such transformative action, Pakistan risks relegating itself to perpetual dependencya nation forever teetering on the edge of crisis, yet never daring to leap toward meaningful reform.

This article was published by the Indian Council of World Affairs in the book titled: The Downfall

Of The State Of Pakistan: A Decade Of Decadence And Degeneration

This article was published by the Indian Council of World Affairs in the book titled: The Downfall

Of The State Of Pakistan: A Decade Of Decadence And Degeneration

References

| [1] | “Rupee ends 2024 on strong note,” [Online]. Available: https://tribune.com.pk/story/2519150/rupee-ends-2024-on-strong-note. |

| [2] | “Reserves soar to $10.7 billion,” [Online]. Available: https://tribune.com.pk/story/2500533/reserves-soar-to-107-billion#google_vignette. |

| [3] | “Pakistan’s FDI Falls 35 % In Nine Months,” [Online]. Available: https://www.businessworld.in/article/pakistans-fdi-falls-35-in-nine-months-387178. |

| [4] | “Tax-to-GDP ratio drastically down in 2023-24,” [Online]. Available: https://www.brecorder.com/news/40331401/tax-to-gdp-ratio-drastically-down-in-2023-24. |

| [5] | “India’s tax to GDP ratio higher than countries at similar income levels,” [Online]. Available: https://www.thehindu.com/business/indias-tax-to-gdp-ratio-higher-than-countries-at-similar-income-levels/article68450116.ece. |

| [6] | “EU: Taxes Accounted For 40% of GDP In European Union In 2023,” [Online]. Available: https://www.ifcreview.com/news/2024/november/eu-taxes-accounted-for-40-of-gdp-in-european-union-in-2023/. |

| [7] | “FAO in Pakistan,” [Online]. Available: https://www.fao.org/pakistan/our-office/pakistan-at-a-glance/en/. |

| [8] | “IMF downgrades Pakistan’s GDP growth outlook for 2025,” [Online]. Available: https://timesofindia.indiatimes.com/world/pakistan/imf-downgrades-pakistans-gdp-growth-outlook-for-2025-to-3/articleshow/117355322.cms. |

| [9] | “IMF The Extended Fund Facility (EFF),” [Online]. Available: https://www.imf.org/en/About/Factsheets/Sheets/2023/Extended-Fund-Facility-EFF. |

| [10] | “2019 PAKISTAN: REQUEST FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY—PRESS RELEASE,” [Online]. Available: https://www.imf.org/-/media/Files/Publications/CR/2019/1PAKEA2019001.ashx. |

| [11] | WTO, “Indonesia: December 1998,” [Online]. Available: https://www.wto.org/english/tratop_e/tpr_e/tp094_e.htm#:~:text=Indonesian%20Economic%20Experience%20in%201997&text=During%20this%20period%2C%20the%20economy,that%20adversely%20affected%20agricultural%20output.. |

| [12] | IMF, “Pakistan: History of Lending Commitments,” [Online]. Available: https://www.imf.org/external/np/fin/tad/extarr2.aspx?memberKey1=760&date1key=2023-08-31. |

| [13] | IMF, “2013 ARTICLE IV CONSULTATION AND REQUEST FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY,” [Online]. Available: https://www.imf.org/external/pubs/ft/scr/2013/cr13287.pdf. |

| [14] | R. Haq, “Pakistan Currency and Foreign Reserves in Sharp Decline,” [Online]. Available: https://www.southasiainvestor.com/2013/12/pakistan-currency-and-foreign-reserves.html. |

| [15] | G. o. Pakistan, “Pakistan Economic Survey 2011-12,” [Online]. Available: https://www.finance.gov.pk/survey/chapter_12/highlights.pdf. |

| [16] | F. A. Khawaja, “Pakistan Real Estate: A Roadmap for Economic Growth,” [Online]. Available: https://avenirdevelopments.com/pakistan-real-estate-roadmap-for-economic-growth/#:~:text=The%20population%20has%20grown%20at,during%20the%20same%20period1.&text=The%20real%20estate%20sector%20contributed,national%20GDP%20in%20FY233.. |

| [17] | S. B. o. Pakistan, “Exploiting Direct Tax Potential in Pakistan,” [Online]. Available: https://www.sbp.org.pk/AnnualRepo/index-4.2.asp. |

| [18] | D. S. Afghan, “The Dark Side of Real Estate: Uncovering its Malevolent Influence on National Economic Progression,” [Online]. Available: https://cdpr.org.pk/wp-content/uploads/2023/07/The-Dark-Side-of-Real-Estate.pdf. |

| [19] | “FOURTH AND FIFTH REVIEWS UNDER THE EXTENDED ARRANGEMENT AND REQUEST FOR WAIVERS OF NONOBSERVANCE OF PERFORMANCE CRIETERIA—STAFF REPORT; STAFF SUPPLEMENT; PRESS RELEASE; AND STATEMENT BY THE EXECUTIVE DIRECTOR FOR PAKISTAN,” [Online]. Available: https://www.imf.org/external/pubs/ft/scr/2014/cr14357.pdf. |

| [20] | “PPP announces countrywide protest against government’s privatisation policy,” [Online]. Available: https://www.brecorder.com/news/4168358/ppp-announces-countrywide-protest-against-governments-privatisation-policy-201402081151123. |

| [21] | “International Monetary Fund Press Release No. 16/373,” [Online]. Available: https://www.imf.org/en/News/Articles/2016/08/04/14/01/PR16373-Pakistan-IMF-Staff-Completes-Twelfth-and-Final-Review-Mission. |

| [22] | “Pakistan Continues Upbeat Growth Prospect, But Challenges Remain,” [Online]. Available: https://www.adb.org/news/pakistan-continues-upbeat-growth-prospect-challenges-remain. |

| [23] | G. o. Pakistan, “Pakistan Debt Policy Statement 2018-19,” [Online]. Available: https://www.finance.gov.pk/publications/DPS_2018_19.pdf. |

| [24] | “Why is Pakistan out of cash again?,” [Online]. Available: https://peoplesdispatch.org/2019/02/21/why-is-pakistan-out-of-cash-again/?__cf_chl_tk=OgWy_TEzH.I2ZzIxiUf_jDZ9FhUO_0RvWuyD7XMpcG0-1743343407-1.0.1.1-azMHQkPwKEaDnOcKZelYSElaYPI6zJkLAN5Q7.cGTSw. |

| [25] | Aljazeera, “IMF board approves $6bn loan package for Pakistan,” [Online]. Available: https://www.aljazeera.com/economy/2019/7/4/imf-board-approves-6bn-loan-package-for-pakistan. |

| [26] | “Fiscal Policy Statement 2019-20,” [Online]. Available: https://www.finance.gov.pk/publications/FPS_2019_2020.pdf. |

| [27] | G. o. Pakistan, “Annual Debt Review & Public Debt Bulletin FY2019-20,” [Online]. Available: https://www.finance.gov.pk/dpco/Annual_Debt_Review_Debt_Bulletin_Jun_2020.pdf. |

| [28] | “PTI govt adds Rs565 billion to circular debt,” [Online]. Available: https://tribune.com.pk/story/2138035/pti-govt-adds-rs565-billion-circular-debt. |

| [29] | “Privatization Plans For Pakistani Power Firms Trigger Anger,” [Online]. Available: https://www.rferl.org/a/water-power-development-privatization-protest-islamabad/31104246.html. |

| [30] | “Imran announces mega relief package,” [Online]. Available: https://tribune.com.pk/story/2345617/imran-announces-mega-relief-package. |

| [31] | IMF, “2024 ARTICLE CONSULTATION AND REQUEST FOR AN EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY—PRESS RELEASE; STAFF REPORT; AND STATEMENT BY THE EXECUTIVE DIRECTOR FOR PAKISTAN,” [Online]. Available: https://www.imf.org/en/Publications/CR/Issues/2024/10/10/Pakistan-2024-Article-IV-Consultation-and-Request-for-an-Extended-Arrangement-under-the-556152. |

| [32] | G. o. Pakistan, “EXECUTIVE SUMMARY: The 13th Five Year Plan (2024-2029),” [Online]. Available: https://uraanpakistan.pk/executive-summary/. |

| [33] | OECD, “Revenue Statistics in Asia and the Pacific 2024- Pakistan,” [Online]. Available: https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/global-tax-revenues/revenue-statistics-asia-and-pacific-pakistan.pdf. |

| [34] | “Pakistan Total External Debt,” [Online]. Available: https://tradingeconomics.com/pakistan/external-debt. |

| [35] | “Power sector circular debt to hit Rs2.8trn despite 51% hike in electricity tariff,” [Online]. Available: https://profit.pakistantoday.com.pk/2024/09/24/power-sector-circular-debt-to-hit-rs2-8trn-despite-51-hike-in-electricity-tariff/. |

| [36] | “Pakistan’s dependence on imported LNG exacerbates energy insecurity and financial instability,” [Online]. Available: https://ieefa.org/articles/pakistans-dependence-imported-lng-exacerbates-energy-insecurity-and-financial-instability. |

| [37] | N. G. Ali, “Land Reforms Are Dead, Long Live Land Reforms: Thoughts on Land Struggles in Pakistan,” [Online]. Available: https://www.jamhoor.org/read/land-reforms-are-dead-long-live-land-reformsthoughts-on-land-struggles-in-pakistan. |

| [38] | “Land Reforms of Zulfikar Ali Bhutto,” [Online]. Available: https://www.paradigmshift.com.pk/land-reforms-pakistan/. |

| [39] | “Pakistan govt announces nearly 15% hike in defence Budget for 2024-25,” [Online]. Available: https://www.business-standard.com/world-news/pakistan-govt-announces-nearly-15-hike-in-defence-budget-for-2024-25-124061201102_1.html. |

| [40] | A. Siddiqa, Military Inc. Inside Pakistan’s Military Economy, London: Pluto Press, 2007. |

| [41] | “The Military and Denied Development in the Pakistani Punjab,” 2014. [Online]. Available: https://www.cambridge.org/core/books/military-and-denied-development-in-the-pakistani-punjab/C43799932CC38A22BD2F80548982363D. |

| [42] | G. o. Pakistan, “Country Wise Net FDI in Pakistan,” [Online]. Available: https://invest.gov.pk/statistics. |

| [43] | “Why Did FDI Inflows of Pakistan Decline? From the Perspective of Terrorism, Energy Shortage, Financial Instability, and Political Instability,” [Online]. Available: https://www.tandfonline.com/doi/full/10.1080/1540496X.2018.1504207? |